Basic features of credit protection insurance

Published on 05. February 2021

Credit Protection Insurance (CPI) is one of the usual instruments of credit insurance (collateral), which banks can require, in accordance with their internal processes and conditions, for the purpose of loan approval. This type of insurance is most often used as collateral when granting housing and consumer (cash) loans to citizens.

The purpose of this product is to ensure the payment of the borrower's credit obligations in the event of their inability to properly repay the debt in certain cases defined in the insurance contract (e.g. job loss, prolonged sick leave, etc.). In this way, banks protect themselves against potential losses in case debtors are unable to properly meet their obligations, as the repayment of the loan to the bank will be done by an insurance company.

Given the significance of this product, it is important that the borrowers are aware of how this insurance serves them so that their credit obligations can be settled for a certain period of time in the event of a repayment problem. It is therefore essential to pore over the terms and conditions of the insurance and, in the event of doubts or uncertainties, contact the bank offering the product or the insurance company and ask for further clarifications.

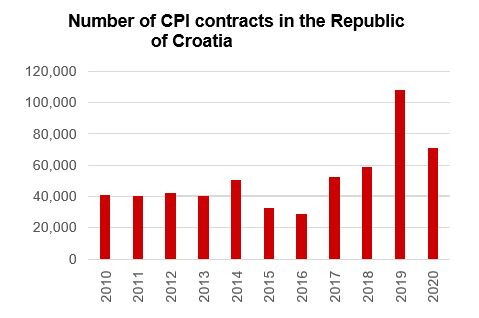

Source: Hanfa

As this is a type of insurance tied to the use of another financial product, the credit activity of banks affects the conclusion of these insurance contracts. It is, therefore, noticeable that since the economic recovery from 2015 and stronger bank lending, the conclusion of these insurance contracts has also increased. Due to the impact of the COVID-19 epidemic on the economy and consequently on the labour market, this trend of new CPI contracting has been halted, while the probability of a larger number of situations in which bank clients, i.e. borrowers, have difficulties in meeting their loan obligations, and therefore more intensive activation of the existing credit protection insurance contracts is increasing.

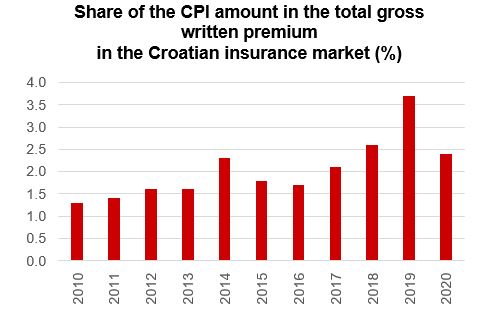

Source: Hanfa

Although this insurance product has a relatively small share in the insurance market in the Republic of Croatia (less than 2.5% of the total amount of the gross written premium), this type of insurance is significant in the context of consumer protection, therefore, informing consumers about this product and its characteristics is very important. In doing so, particular attention should be paid to the coverage, i.e. the situations defined in the credit protection insurance contract.

Each insurance company defines for itself the conditions for ensuring the loan repayment, however, some common situations that may trigger the activation of the contract are temporary incapacity to work, job loss and death.

It is important to note that insurance terms and conditions generally also contain limitations on the obligations of the insurance company. This means that, for example, in case of temporary incapacity for work or unemployment, the company covers a number of monthly credit annuities, i.e. instalments (e.g. for 6 months of unemployment) and the number of risks insured is limited (e.g. not more than two or three such events in the course of the duration of insurance, for example two job losses). In addition, the terms and conditions normally include general exclusions of the insurance company’s obligations, i.e. situations where the insurance company is not obliged to assume the payment of the credit obligation (e.g. certain health status of the insured person before the start of insurance, consumption of alcohol or drugs, participation in criminal offences, etc.). Moreover, the terms and conditions of the contract generally include exclusions relating to a particular risk or coverage. For example, in the case of unemployment of the insured person, the insurance company can only consider the situations where the insured person did not quit the job themselves, when the dismissal occurred without fault of the insured person, when the insured person was registered as an unemployed person in the records of the Croatian Employment Service, etc.

Therefore, it is very important for the insured person to be informed before signing/concluding the contract about the cases of so-called “limitations and exclusions”, that is, about the cases and events in which the insurance company is not obliged to assume the obligations of the loan. This can help prevent any disputes between the insured person and the insurance company, and Hanfa knows from practice that disputes in this type of insurance are most common precisely about the time when the insured case occurred. These examples of coverage and general and specific exclusions are only informative and generalised, and may vary under the conditions of various insurance companies.1

Can a bank requesting CPI to grant a loan sell CPI at the same time?

It is often the case that a bank has established a business relationship and cooperation with one or more insurance companies and, for the sake of the efficiency and simplicity of the loan approval process, it may offer a future borrower to conclude a CPI contract with one of these companies. In such cases, the bank usually also acts as an insurance distributor. The register of banks acting as insurance distributors and agents and the list of insurance companies represented by every bank are available on Hanfa’s website. While Hanfa is not the authority responsible for the topic of credit granting and cannot provide opinions on what documentation a particular bank requires in the credit granting process, please note that a bank should not demand from future borrowers to conclude a CPI contract with a particular insurance company and that, as a general rule, the client may decide independently on the choice of the insurance company, as long as the insurance protection offered by such insurance is in line with the bank's terms and conditions for credit granting. Cases where a bank client concludes a CPI contract for the purpose of obtaining a loan do not constitute mis-selling, as this is precisely the insurance type/service connected with the “main” financial product (loan).

1 As mentioned above, insurance companies draw up the insurance terms and conditions independently. These terms and conditions are not subject to prior approval by Hanfa. Hanfa is not part of the judicial authority and, in the event of a dispute between contracting parties, cannot arbitrate and establish the correctness of the interpretation of a definition, limitation or exclusion from the terms and conditions of an insurance contract. Therefore, all potential borrowers whose bank requires them to conclude a CPI contract are instructed to be informed in a timely and detailed manner about the terms and conditions of the insurance contract.