Macroprudential Risk Scanner

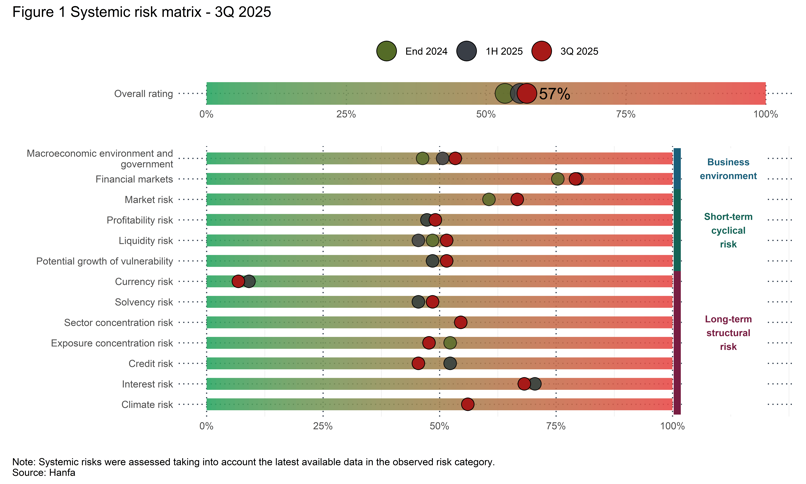

The level of systemic risks in the financial services sector decreased slightly in the third quarter of 2024. Mitigated inflationary pressures and resilience of the global economy reduced systemic risks stemming from the international macroeconomic environment. Although pronounced growth in real estate prices remains a prominent short-term risk, resilient economic growth and improved public finance indicators led to an upgrade in Croatia’s credit rating, which further diminished systemic risks arising from the domestic economy. In the financial environment, the shift in the monetary policy stance and optimistic investor sentiment had a positive impact on valuations, as was reflected in the recovered profitability of the sector in the third quarter of 2024.

However, interest rate risk and related market risks remain the key risks for the domestic financial services sector. Structural characteristics of the domestic financial services sector, such as the concentration of institutional investors’ exposure and low activity in the domestic capital market, have shown some improvements, but could still further exacerbate the sector’s losses should the subdued global risk premium increase. The sector’s liquidity and solvency buffers are holding steady at high levels, providing additional hedge against sudden shocks. Despite a slight decrease, systemic risks in the financial services sector remain elevated due to pronounced cyclical risks in the financial environment, including geopolitical uncertainties and relatively high market valuations that increase the probability and potential impact of a highly unlikely but plausible systemic shock.

The publication Macroprudential Risk Scanner provides insight into the process of identifying, assessing and monitoring the evolution of systemic risks in the financial services sector under Hanfa’s supervision, in order to timely take appropriate measures to prevent their materialisation and the impairment of the financial system stability. The objective of the publication is to contribute to a better understanding of systemic risks, stimulate action planning and measures that prevent the materialisation of such risks and provide adequate protection against the consequences of their materialisation with the aim of strengthening the system's resistance to shocks, as well as to contribute to greater confidence in the financial system. The Macroprudential Risk Scanner is published four times in a year.

")