January 2026 Monthly Report

Overview of supervised entities’ activities in the financial services sector for January 2026

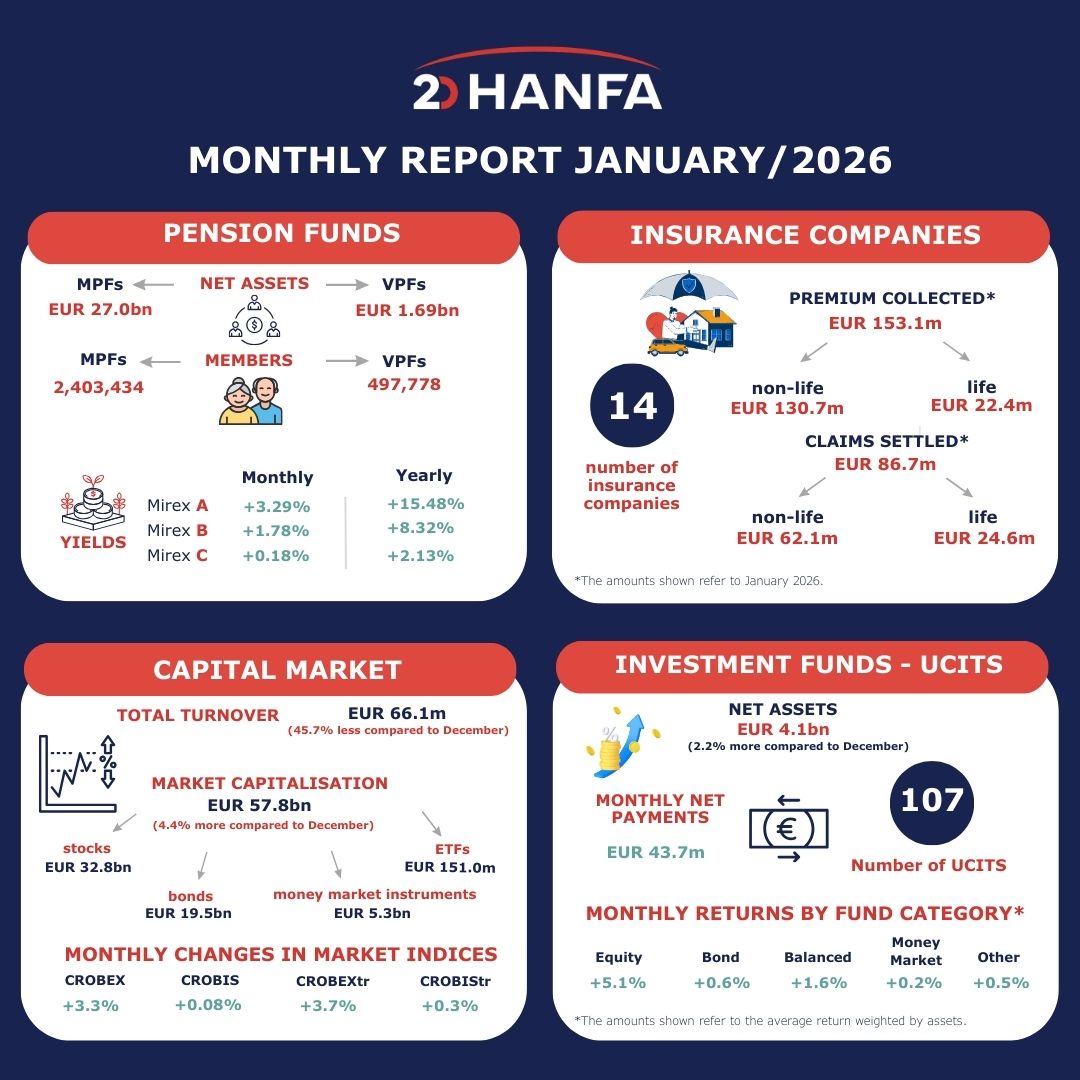

PENSION FUNDS

SECOND PILLAR PENSION FUNDS

At the end of January 2026, mandatory pension funds (MPFs) had 2,403,434 members, i.e. 3,254 (0.14%) members more than in the previous month. Category B funds had 74.60% of all MPF members, while category A and category C funds had 22.03% and 3.36% of all MPF members respectively. Out of 4,466 new members, 4,169 (93.4%) were automatically assigned by Regos. Termination of membership due to retirement or death was recorded with respect to 1,212 insured persons. Total net contributions paid to MPFs amounted to EUR 143.5m (0.5% of net assets at end-December). At the same time, total payments from all MPFs due to personal account closures reached EUR 28.7m (0.1% of net assets at end-December), falling by EUR 27.1m (48.5%) compared to the previous month.

At the end of January 2026, MPFs’ net assets amounted to EUR 27.0bn, rising by EUR 553.6m (2.1%) relative to the previous month. Nominal monthly Mirex returns reached 3.29% for category A[1], 1.78% for category B and 0.18% for category C. Annual Mirex returns reached 15.48% for category A, 8.32% for category B and 2.13% for category C, while annualised[2] returns since the beginning of MPFs’ operation reached 8.68% for Mirex A, 5.60% for Mirex B and 3.24% for Mirex C[3].

At the end of January, bond investments of MPFs totalled EUR 15.0bn (55.5% of total assets), making their share decrease by 0.77 p.p. on a monthly basis. The share of equity investments in MPFs’ assets increased by 0.6 p.p. on a monthly basis, amounting to 25.0% of MPFs’ assets (EUR 6.8bn) at the end of January. Investments in domestic shares accounted for 14.1%, while investments in foreign shares accounted for 10.9% of MPFs’ assets. Investments in investment funds amounted to EUR 2.9bn (10.9% of the assets), making the proportion of these investments in total assets increase by 0.2 p.p. relative to the previous month. Cash and deposits amounted to 6.2% of the assets, or EUR 1.7bn, decreasing by 0.2 p.p. on a monthly basis.

THIRD PILLAR PENSION FUNDS

At the end of January 2026, the number of members of 8 open-ended voluntary pension funds (OVPFs) rose by 0.58% on a monthly basis, while the number of members of 21 closed-ended voluntary pension funds (CVPFs) increased by 0.16%, making the number of members of these funds reach 419,006 and 51,080 respectively. Total monthly payments made to voluntary pension funds (VPFs) in January 2026 amounted to EUR 15.2m (0.9% of net assets at end-December), decreasing by 69.0% compared to the previous month. Total payments made from these funds reached EUR 7.8m, increasing by 37.5% on a monthly basis. Total payments from VPFs made due to retirement and other reasons accounted for 60.1%, payments made due to the change of fund reached 36.0%, while those made due to death accounted for 3.9% of total payments in January. As regards total payments made due to retirement, the amount of EUR 1.8m was paid through a pension company (fund), EUR 1.5m was paid in the form of lump-sum payments, while the amount of EUR 1.3m was transferred for payment to pension insurance companies.

In January, VPFs’ net assets increased by EUR 31.3m (1.9% on a monthly basis) and stood at EUR 1.69bn. Monthly nominal returns of VPFs ranged from 0.2% to 3.7%. As regards the investment structure of VPFs, the largest part of the portfolio was made up of bonds and amounted to a 51.2% share in total net assets, followed by stocks with a 29.0% share and investment funds with a 9.2% share. The share of bonds and investment funds in VPFs’ investments decreased on a monthly basis by 1.1 p.p. and 0.5 p.p. respectively, while the share of stocks rose by 0.8 p.p.

PENSION INSURANCE COMPANIES (PICs)

At the end of 2025, there were two pension insurance companies operating on the market and covering 22,732 and 4,108 users in the segment of mandatory and voluntary pension insurance respectively. Total assets of the PICs amounted to EUR 700.3m at the end of 2025, rising by EUR 142.8m or 25.6% compared to the same period of the previous year. The total profit of the PICs in 2025 amounted to EUR 1.3m, decreasing by EUR 635 thousand (33.6%) compared to the same period last year.

INSURANCE COMPANIES

In January 2026, there were 14 insurance companies operating on the market. Their total premium collected in the first month of 2026 amounted to EUR 153.1m, i.e. 0.3% less than in the same period in 2025. EUR 22.4m (14.6%) of this amount related to life insurance premium (1.7% less than in the same period last year), while EUR 130.7m (85.4%) related to non-life insurance premium (0.1% less at an annual level). The structure of the non-life insurance premium collected is dominated by motor vehicle liability insurance (35.9%), followed by insurance of road vehicles (20.2%), health insurance (10.0%), and insurance against fire and natural disasters (9.4%). The amount of claims settled in January 2026 reached EUR 86.7m, decreasing by 5.7% compared to same period in 2025. EUR 24.6m (28.3%) of this amount related to life insurance (3.2% less at an annual level), while EUR 62.1m (71.7%) related to non-life insurance (6.6% less compared to the same period in 2025). In the total amount of claims settled in non-life insurance, the largest amounts related to motor vehicle liability insurance (40.6%), insurance of road vehicles (21.6%), health insurance (13.3%), and insurance against fire and natural disasters (6.97%).

CAPITAL MARKET

In January 2026, the total turnover on the Zagreb Stock Exchange reached EUR 66.1m, decreasing by 45.7% on a monthly basis. Market capitalisation increased by 4.4% relative to the previous month and stood at EUR 57.8bn, of which stocks amounted to EUR 32.8bn, bonds to EUR 19.5bn, money market instruments to EUR 5.3bn and ETFs to EUR 151m. As regards sectoral stock indices, the largest monthly growth (8.6%) was recorded by CROBEXkonstrukt, while CROBEXtransport recorded the smallest monthly rise (0.04%). The main ZSE stock index CROBEX recorded a monthly increase of 3.3%, whereas CROBEXtr rose by 3.7% on a monthly basis. As regards bond indices, CROBIS recorded a 0.08% monthly increase, while CROBIStr grew by 0.3% at an annual level. KONČAR d.d. was once again the stock most traded in January, with its turnover amounting to EUR 18.9m (38.1% of the overall trade in stocks in January) and an 11.7% monthly price increase.

INVESTMENT FIRMS

At the end of the fourth quarter of 2025, there were 22 legal entities authorised to provide investment services, namely 7 investment firms, 11 credit institutions and 4 investment fund management companies. The value of assets managed by investment firms rose by 18.5% on a quarterly basis, the value of assets managed by credit institutions increased by 7.3%, while the value of assets managed by investment fund management companies declined by 0.03%. At the end of the fourth quarter of 2025, total assets under custody of investment firms stood at EUR 1.7bn, a 5.5% increase on a quarterly basis, while the assets under custody of credit institutions increased by 3.4%, reaching EUR 30.3bn.

At the end of January 2026, there were 107 UCITS operating on the market. Their total net assets amounted to EUR 4.1bn, increasing by EUR 90.4m (2.2%) compared to the previous month. Total monthly net payments to UCITS in January were positive, amounting to EUR 43.7m. Positive net payments were recorded by equity funds (EUR 34.4m), money market funds (EUR 10.3m), and other funds (EUR 1.8m), while negative net payments were recorded by feeder funds (EUR -0.3m), bond funds (EUR -0.6m) and balanced funds (-1.8m).

Money market funds’ net assets accounted for 34.9% of the total net assets of all UCITS at the end of January, bond funds made up 21.8%, equity funds accounted for 22.3%, other funds for 15.2%, while balanced funds and feeder funds made up 3.6% and 2.2% of the total UCITS’ net assets respectively. All UCIT categories recorded positive asset-weighted monthly returns, namely equity funds (5.1%), balanced funds (1.6%), feeder funds (1.1%), bond funds (0.6%), other funds (0.5%) and money market funds (0.2%).

The assets of the Fund for Croatian Homeland War Veterans and Members of their Families amounted to EUR 219.0m (a 1.7% monthly decrease), with the monthly return of the fund reaching -1.53%.

LEASING COMPANIES

At the end of 2025, there were 15 leasing companies operating on the market. Their total assets stood at EUR 4.5bn, a 10.1% increase compared to the end of the previous year. At the same time, the total profit recorded by leasing companies rose by 10.0% on an annual basis, reaching EUR 55.3m. The outstanding contract value of active contracts in the operating lease segment rose by 1.6% at an annual level, while in the finance lease segment it increased by 11.8%. The value of newly concluded contracts in 2025 decreased by 6.8% at an annual level in the operating lease segment, while the annual growth in the finance lease segment reached 5.9%.

FACTORING COMPANIES

At the end 2025, there were three factoring companies operating on the market. Their total assets stood at EUR 21.5m, while their profit reached EUR 0.8m. In 2025, their transaction volume was dominated by classic factoring totalling EUR 104.3m (82.3% of all the transactions), as were receivables, with classic factoring amounting to EUR 13.7m (78.4% of all the receivables) at the end of the year.

The full report is available at Statistics/Monthly reports.

1 In January 2026, the monthly change recorded by the Mirex index for category A was higher than the highest return among the category A funds in the period observed. This is a consequence of the methodological approach to constructing the Mirex index, which represents the average value of the accounting unit of all mandatory pension funds in the same category (A, B or C), with the units of each fund in the total net assets of the funds in that category used as weights in the calculation. Therefore, the Mirex index return represents the change in two weighted averages of unit prices at different points in time, rather than a weighted average of the individual fund returns. It is therefore possible for the Mirex index return over a given period to be higher than the return of any individual fund; such a situation may occur when in the observed period, one of the funds, due to its significantly larger assets and unit price compared to the other funds, also records a relatively faster growth in its assets and unit price, thus exerting the strongest impact on the movement of the Mirex A index value, as well as on the magnitude of the change in the index.

[2] The annualised return is the geometric average of annual returns realised in the period observed.

[3] Beginning of operation: MPF category B: 30/4/2002; MPFs category A and C: 21/8/2014