Financial education: What is a bond?

Published on 22 February 2023

For the first time, the so-called “national bond” will be issued in Croatia. It is a government bond issued by the Ministry of Finance, that will be able to be directly purchased by citizens, as retail investors. So far, government bonds as an investment form have been available only to financial institutions, while citizens were able to participate in the government bond market indirectly, by acquiring a unit in an investment fund or through pension savings. Given that there could be increasing interest of citizens in this kind of investment, the following text provides some basic features of investments in bonds, irrespective of their issuer.

A bond is a long-term debt security that may be issued by governments and government institutions, local and regional self-government units or companies. Bond investment is similar to regular bank savings in some of its characteristics. For example, by purchasing a bond, the buyer lends the money to the bond issuer for a fixed period of time. Upon the expiry of this period of time, the buyer receives back the original amount increased by interest. The interest rate paid on a bond is called the coupon and it does not change until the maturity date, that is, the date when the bond issuer must pay off the bond. Bonds are therefore a type of investment that generates a fixed interest income. In general, the interest is paid periodically, usually on a semi-annual or annual basis, and it is a continuous source of inflows, similar to the bank savings interest. Issues of bonds whose interest is added to the principal and paid upon maturity are less frequent.

|

Coupon |

Interest rate paid on a bond |

|

Nominal value |

The value of a bond at its issue date |

|

Maturity |

The date on which a bond falls due; bond's principal is repaid with interest to the bond holder |

|

Transferability |

The possibility of selling the bond on the financial market prior to its maturity date |

|

Capital gains/losses |

The sale of a bond prior to its maturity may result in a gain (if the bond is sold at a price higher than its nominal value), or in a loss (if the bond is sold at a price lower than its nominal value) |

Bonds are regularly issued by governments and government institutions and investments in such issues generally involve the lowest levels of risk. Bonds may also be issued by local and regional self-government units, as well as companies, which use them in order to borrow money needed for their business operations without changing their ownership structure.

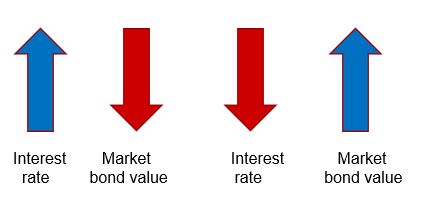

Unlike bank savings, bonds are transferable and may be sold on the financial market even prior to their maturity. The sale of a bond prior to its maturity may result in a gain, but also in a loss, depending on its current market price, which may be higher or lower than the initial purchase price, that is, its nominal value. The market price of a bond depends on market interest rate movements: rising interest rates generally lead to rising returns, that is, gain on new investments (e.g. a new bond issued at a higher interest rate or a new bank deposit that has a higher interest rate), which, as a rule, reduces the investment appeal of previously issued bonds whose interest rates are fixed. Less attractive bonds lead to a decrease in their market price. The situation is opposite in the case of falling interest rates on the market, when market prices of previously issued bonds generally rise. Interest rates (yields) and market bond prices are therefore said to be inversely related.

Bonds can be sold prior to their maturity date on the so-called secondary market (this can be the regulated market of the Zagreb Stock Exchange or the so-called OTC market). In this case, bond holders cannot sell their bonds directly by themselves; instead, this is done through the investment firms on the basis of the contract concluded, for which the bond holders pay certain transaction costs. There is also a possibility of selling bonds directly via the purchase agreement between the seller and the buyer, as for any other type of assets.

Depending on the type of bond and holding period, a bond can produce income for the investor in two ways:

- current income in the form of the accrued interest (the so-called interest income)

- possible gains as a result of the increasing bond market value relative to its nominal value (the so-called capital gains); however, investors can also experience losses in the case where the market value of the bond declines (the so-called capital losses).

Capital gains in Croatia are taxed at a 10% rate, with surtax also being levied, but only if capital gains have been generated within the period of two years following the investment. That means that capital gains are not taxed if the duration of the bond investment is longer than two years or if the bond is held until maturity. Interest income from bond investments is not subject to tax.